Naimish Keswani

July 9, 2021

Mutual fund sponsors this year have successfully converted their products into ETFs for the

first time since the Securities and Exchange Commission approved the ETF rule in 2019,

eliminating the need for exemptive relief and removing barriers to entry.

Guinness Atkinson Funds, Starboard Investment Trust, and Dimensional Funds are among

the first to have managed mutual fund-to-ETF conversions, paving the way for others.

Before a mutual fund can be converted, the process must be approved by the fund’s board,

which means independent directors should question the adviser about the motivations for

the transaction and its impact on shareholders, according to Brian McCabe, partner at Ropes

& Gray.

One typical reason why an adviser may want to convert a mutual fund is to take advantage

of a perceived opportunity in distributing the strategy in an ETF wrapper instead.

“They think that potential customer base is more interested in an ETF solution than it is in

the form of a traditional mutual fund,” he says.

According to the Investment Company Institute, overall demand for mutual funds lagged

demand for ETFs in 2020, with the former seeing $205bn in net inflows while the latter saw

$501bn.

Tax benefits associated with ETFs are another reason why sponsors are making the jump. Tax

efficiency was one of the key reasons for Dimensional to convert four of its equity mutual

funds, which held $28.8bn in assets.

“The additional benefits that an ETF brings to the table in terms of in-kind create-redeems

will help us improve our tax efficiency further,” said Gerard O’Reilly, Co-CEO and CIO at

Dimensional Fund Advisors in an interview with Bloomberg.

“Taxes are on a lot of investors’ minds these days, so we think it is a good thing for the

shareholders of those funds.”

Custom baskets under rule 6c-11 also aid tax efficiency, as the ETF will not have to recognize

capital gains on appreciated securities within the custom redemption basket, allowing

shareholders to delay taxable gains to when they sell the ETF.

“Generally, ETFs also have lower operational expenses as there is no state registration fees

required because they trade on an exchange like a security,” says Tracie Coop, general

counsel at The Nottingham Company, which facilitated the conversion of Starboard

Investment Trust’s Adaptive Growth Opportunities Fund into an ETF.

Conversions may not be appropriate for all mutual funds, however. Funds with large

proportions of 401(k) holders, for instance, may be better off remaining in their current

wrappers.

“The way the regulations are, ETFs are not widely held in 401(k) plans, so if that is your

shareholder market, then an ETF probably is not right for you because those shareholders

will have to exit the funds,” Coop says.

Boards should also consider whether the fund will convert to a transparent ETF or a nontransparent

ETF, as different strategies have different sensitivities, according to McCabe.

“If you’re a portfolio manager who buys based on signals that require you to act really

quickly, and that anybody else could act on, you might not want a transparent ETF because

as soon as people know what you’re buying, they’ll jump ahead of you, and there goes your

secret sauce,” he says.

Non-transparent ETFs also require an exemption from the SEC, which can be restrictive for

some funds, as the SEC says they must be limited to listed US equities and securities that

trade during US market hours.

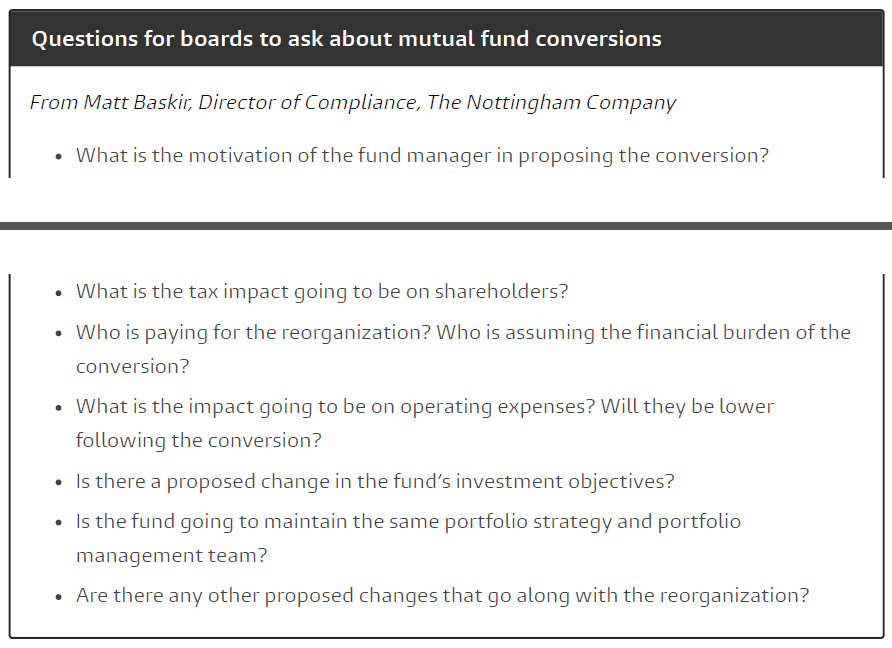

Evaluating Proposals

While evaluating a proposed conversion, boards must investigate to see whether a

conversion is best suited for a particular fund, says Matt Baskir, director of compliance at

Nottingham.

“One of the key benefits is a general reduction in operating expenses, as there are lower

operating expenses for ETFs versus mutual funds. What is the impact going to be on

operating expenses? That is an important question to ask,” he says.

Boards should also discuss the costs of reorganization, as the conversion requires legal

work, multiple regulatory filings, and discussions with the SEC.

“The adviser bearing these costs has been a critical component for board approval, as it isn’t

really appropriate to ask shareholders to bear these costs,” Coop says.

Boards must have confidence in the abilities of service providers and advisers to satisfy dayto-

day requirements, according to Baskir.

“They also have to be confident in the team that they have in place to satisfy requirements

under the ETF rule, in terms of data disclosure, website operations, managing basket

procedures, having internal controls on the adviser level, address board reporting

requirements, annual audit requirements, and things of that nature.”

The Conversion Process

There are two main approaches available to mutual funds, based on their structure and

operations: a direct conversion, and a merger or asset sale conversion.

In a direct conversion, which may require shareholder approval, a mutual fund converts into

an ETF by amending its registration statement and organizational documents, and by

adjusting its operations accordingly.

In a merger or an asset sale, the adviser creates an SEC-registered shell ETF that mirrors the

existing mutual fund. The mutual fund then merges into the ETF.

According to rule 17a-8, a merger between a mutual fund an affiliated ETF is permitted if

their advisory agreements and fundamental policies are not materially different.

“For the (Starboard) Adaptive Growth Opportunities Fund, we did a shell conversion, and

that’s generally a tax-free reorganization,” Coop says.

“The only things that are different now are things that change from a mutual fund to ETF

perspective, such as some additional risks, and now the shareholders are buying through a

broker instead of directly from the fund,” she says.

A conversion is also a cost-efficient way of porting over to ETFs, as starting from scratch

requires raising assets. Certain platforms also require funds to have a certain track record

and history, and conversions are a good way of providing that, according to Coop.

In terms of board oversight, there are a few areas where additional education might be

necessary.

“There are just a few areas where additional reporting to the board may be necessary, some

additional education from the board’s perspective on different potential risks or different

potential operational issues that can arise,” Coop says.

“But overall mutual funds and the oversight of the ETFs are very similar.